The Real Cost of Benchmarking FESE De La Vega Prize '26 FIRS PhD Paper Prize '25 SFS Cavalcade PhD Student Award '25

Abstract

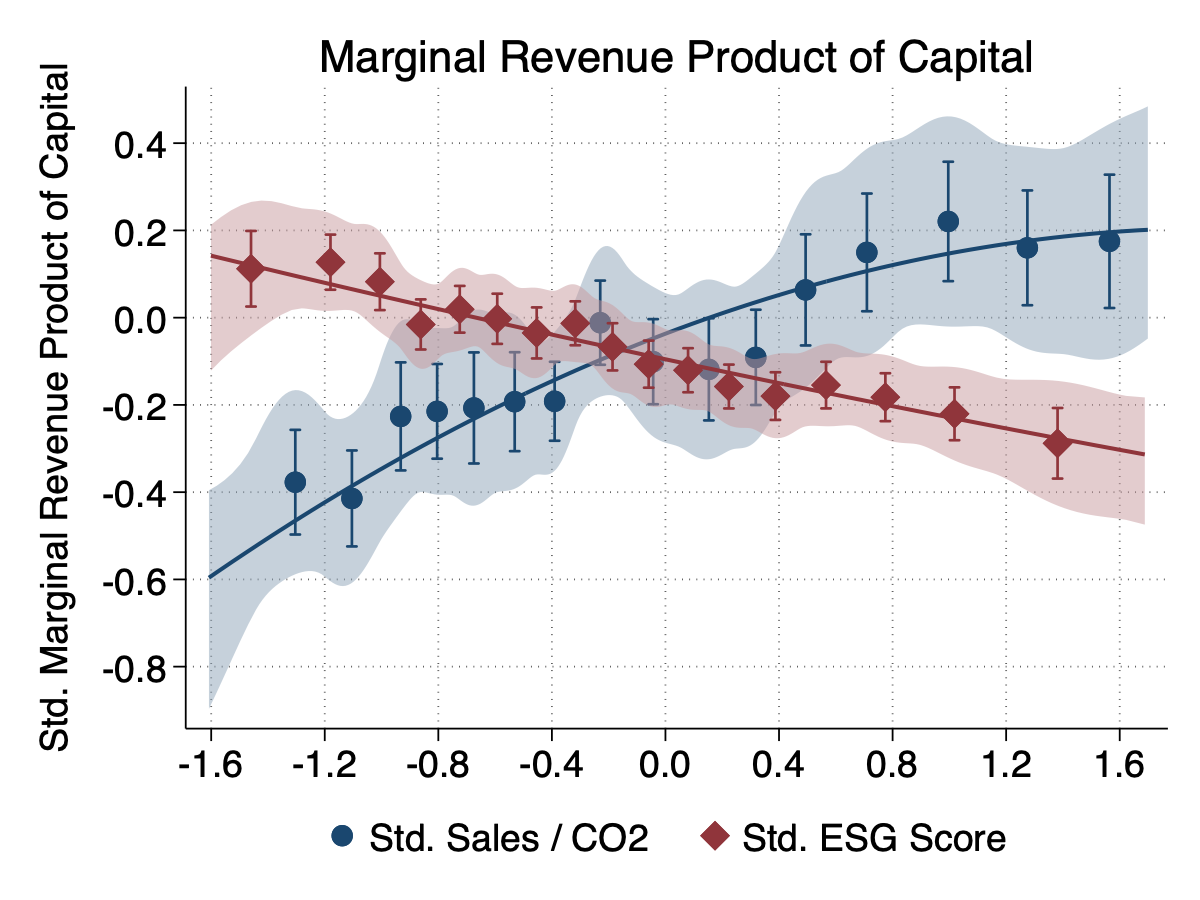

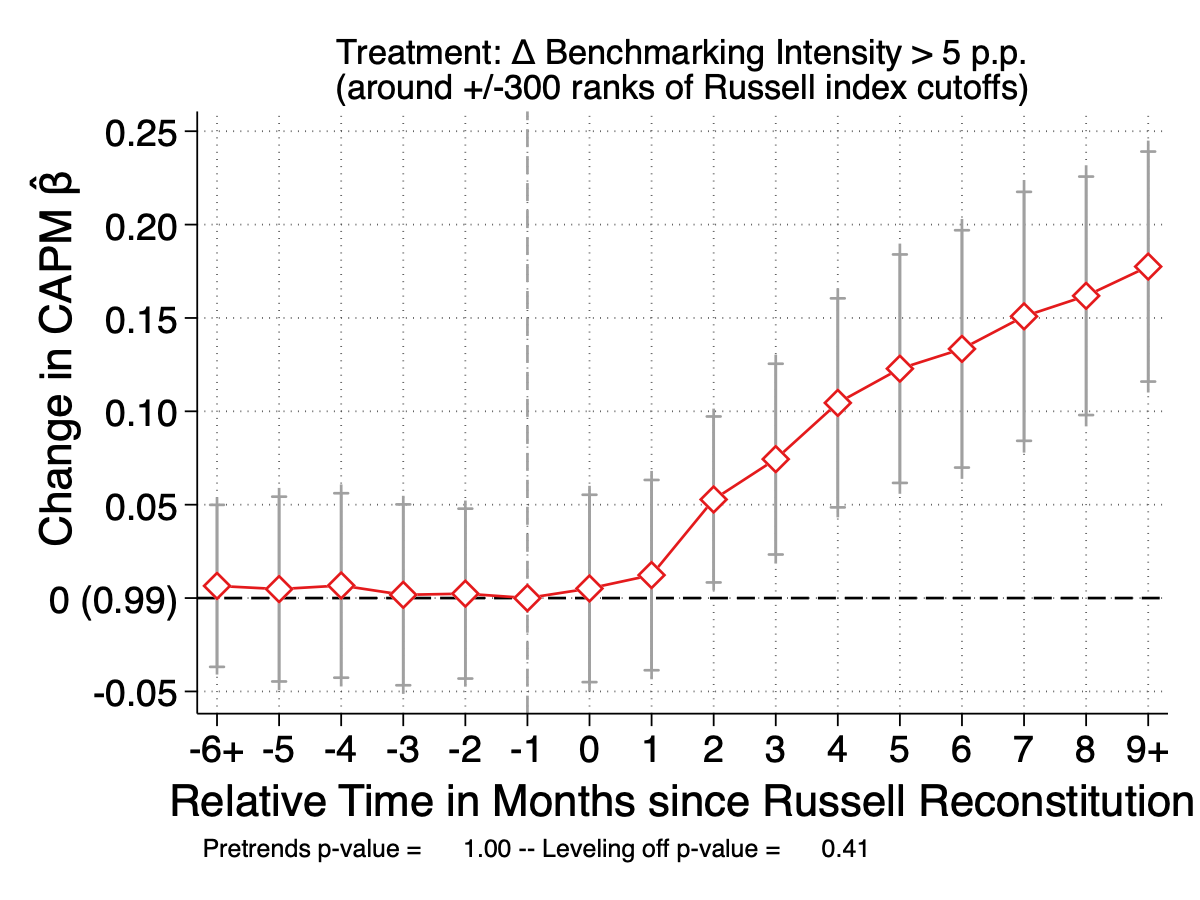

Benchmark-linked capital flows increase firms' CAPM βs, thereby raising managers' perceived cost of equity and reducing investment. Using exogenous variation from Russell and S&P 500 reconstitutions, we show that inclusion in a benchmark stock index increases a stock's CAPM β. Managers interpret the higher β as a higher cost of equity and reduce investment. Consistent with this mechanism, benchmark inclusion also raises the perceived cost of equity among stock analysts and regulators. Industries with larger increases in βs due to benchmarking have accumulated less capital over the past two decades. Benchmark-induced changes in the cross-section of CAPM βs do not cancel out but affect aggregate investment because higher βs fall on many firms with high investment elasticities, while lower βs benefit a few large but inelastic firms.

Seminars: Federal Reserve Bank of New York*, Notre Dame Mendoza, NYU Stern, UT Austin McCombs, Boston College Carroll, Ohio State University Fisher, Bocconi University, University of Virginia Darden, National University of Singapore, Einaudi Institute, Copenhagen Business School, University of Maryland Smith, Singapore Management University

Conferences: EUROFIDAI Paris December Meeting 2026*, EFA Annual Meeting 2026*, AFA Annual Meeting 2026, SFS Cavalcade 2025, FIRS 2025,

Johns Hopkins Carey Finance Conference,

Four Corners/FMRC Conference on Indexing, Investment Company Institute, Northeastern University Finance Conference 2025, UIC Finance Conference 2025c

(* scheduled, c co-author)

Awards: FESE De La Vega Prize 2026, SFS Cavalcade PhD Student Award, FIRS Conference 2025 Prize for PhD Students, Shortlisted for Brandes Center Prize

Media: Bloomberg's Matt Levine Money Stuff, Frankfurter Allgemeine, UC San Diego Brandes Center